JAKARTA, opinca.sch.id – Interest Rate Swaps: Managing Fluctuating Financial Costs might sound super technical, but honestly, once you get it, it can be a lifesaver. Been there, scratching my head the first time my banker threw the term at me! Let me break it down so you get the inside scoop—without the boring bits.

In today’s volatile financial landscape, managing costs effectively is crucial for businesses and investors. One financial instrument that has gained prominence for its ability to mitigate interest rate risk is the interest rate swap. This article explores the mechanics of interest rate swaps, their benefits, and how they can be utilized to manage fluctuating financial costs in unpredictable times.

1. Understanding Interest Rate Swaps

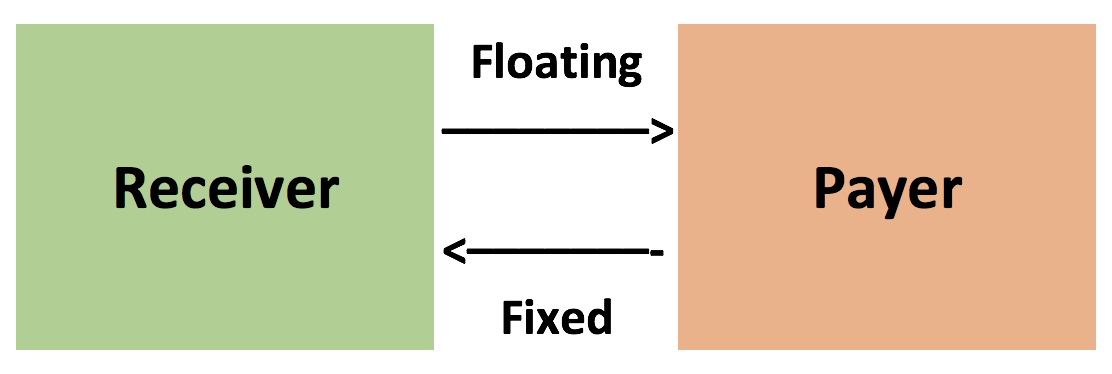

An interest rate swap is a financial derivative contract in which two parties agree to exchange interest rate cash flows based on a specified notional amount. These cash flows typically involve one party paying a fixed interest rate while the other pays a floating interest rate. The primary purpose of an interest rate swap is to manage exposure to fluctuations in interest rates.

Key Components of Interest Rate Swaps

- Notional Principal: The hypothetical amount used to calculate interest payments, which is not exchanged between the parties.

- Fixed Rate: The interest rate that remains constant throughout the life of the swap.

- Floating Rate: The interest rate that fluctuates based on a reference rate, such as LIBOR (London Interbank Offered Rate) or SOFR (Secured Overnight Financing Rate).

- Swap Term: The duration of the swap agreement, which can range from a few months to several years.

2. Benefits of Interest Rate Swaps

Interest rate swaps offer several advantages for businesses and investors looking to manage their financial costs:

– Hedging Against Interest Rate Risk

One of the primary benefits of interest rate swaps is their ability to hedge against rising interest rates. For example:

- Fixed Rate Payers: Companies with floating-rate debt can enter into a swap to pay a fixed rate, protecting themselves from potential increases in interest rates.

- Floating Rate Payers: Conversely, businesses expecting declining rates may choose to pay a floating rate, benefiting from lower costs.

– Improved Cash Flow Management

Interest rate swaps can enhance cash flow predictability by stabilizing interest expenses. This predictability allows businesses to:

- Budget More Effectively: With fixed payments, organizations can plan their finances with greater accuracy.

- Reduce Financial Uncertainty: Minimizing fluctuations in interest expenses can lead to improved financial stability.

– Customization and Flexibility

Interest rate swaps can be tailored to meet the specific needs of the parties involved. This customization includes:

- Notional Amounts: Swaps can be structured around any notional amount, allowing businesses to align the swap with their specific exposure.

- Payment Frequency: Parties can negotiate the frequency of interest payments, which can be monthly, quarterly, or annually.

3. How Interest Rate Swaps Work

To illustrate how interest rate swaps function, consider the following example:

- Company A has a $10 million loan with a floating interest rate tied to LIBOR. Concerned about rising rates, they enter into a swap with Company B, which agrees to pay a fixed rate of 3% on the notional amount of $10 million.

- In exchange, Company A will pay Company B a floating rate based on LIBOR plus a spread (e.g., LIBOR + 1%).

Cash Flow Illustration

Assuming LIBOR is currently at 2%, the cash flows would be as follows:

- Company A pays: LIBOR + 1% = 3% on $10 million → $300,000 annually

- Company B pays: Fixed rate of 3% on $10 million → $300,000 annually

In this scenario, if LIBOR rises to 4%, Company A benefits from the swap because they continue paying the fixed rate while Company B pays the higher floating rate.

4. Managing Risks Associated with Interest Rate Swaps

While interest rate swaps can effectively manage financial costs, they also come with risks that need to be addressed:

– Counterparty Risk

The risk that one party in the swap agreement may default on its obligations can impact the effectiveness of the swap. To mitigate this risk:

- Credit Assessments: Conduct thorough credit assessments of potential counterparties before entering into a swap.

- Collateral Agreements: Consider requiring collateral to secure the obligations of both parties.

– Market Risk

Fluctuations in interest rates can affect the value of the swap. To manage market risk:

- Regular Monitoring: Continuously monitor interest rate movements and assess the impact on the swap’s value.

- Exit Strategies: Have a clear exit strategy in place if market conditions change significantly.

5. Conclusion

Interest rate swaps are powerful financial tools that can help businesses manage fluctuating financial costs in unpredictable times. By understanding how these instruments work and leveraging their benefits, organizations can hedge against interest rate risk, improve cash flow management, and customize solutions to meet their specific needs.

As the financial landscape continues to evolve, interest rate swaps can provide a strategic advantage for those looking to stabilize their financial position. However, it is essential to remain aware of the associated risks and implement appropriate risk management strategies to maximize the effectiveness of these instruments. By doing so, businesses can navigate the complexities of interest rates and ensure long-term financial success.

Boost Your Competence: Uncover Our Insights on Financial

Spotlight Article: “Finance: Strategies for Managing Residential Investments!