Annuity types represent a diverse range of financial products designed to provide a steady income stream, typically during retirement. Understanding the various types of annuities is crucial for individuals looking to secure their financial future. This guide will explore the different annuity types, their features, benefits, and considerations to help you make informed decisions about your financial income stream.

1. What is an Annuity?

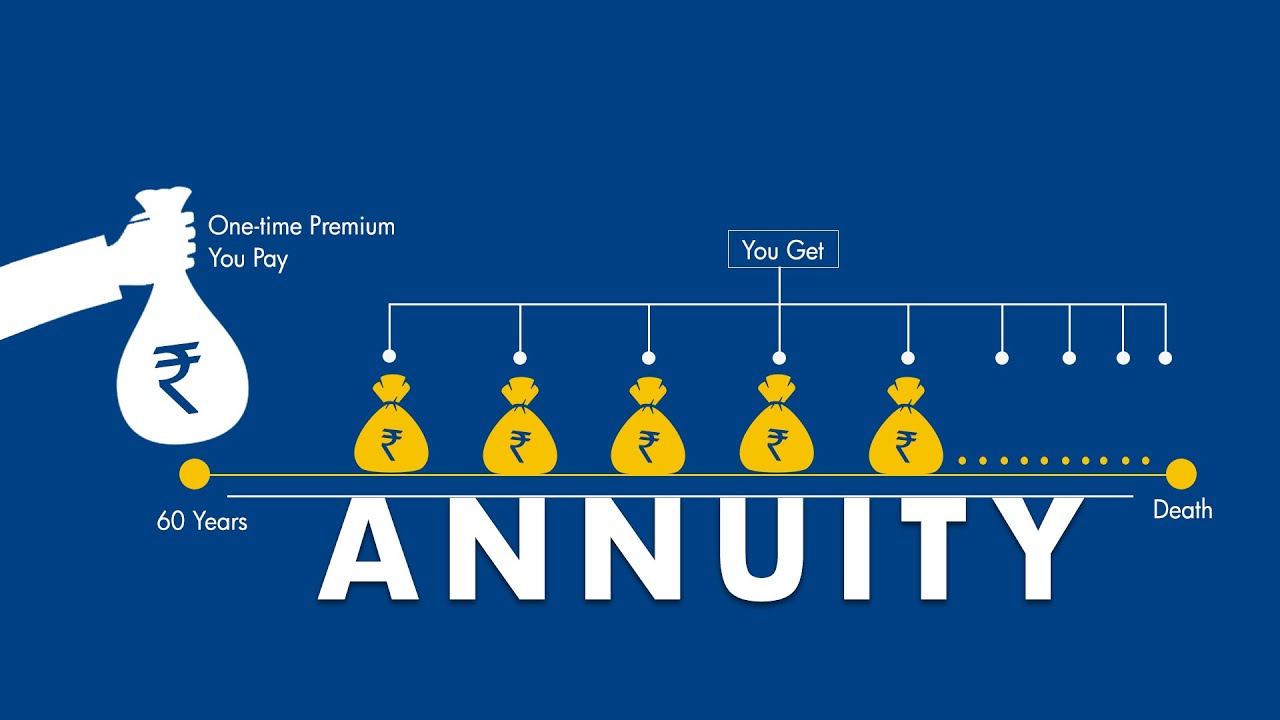

An annuity is a financial contract between an individual and an insurance company that provides regular payments over a specified period or for the lifetime of the annuitant. Annuities are often used as a way to generate income during retirement, allowing individuals to convert a lump sum of money into a predictable income stream.

2. Common Types of Annuities

There are several annuity types, each with unique features and benefits. Understanding these types can help you choose the right one for your financial needs.

a. Fixed Annuities

Fixed annuities provide a guaranteed interest rate and fixed payments over a specified period or for the lifetime of the annuitant. They are considered low-risk investments and are suitable for individuals seeking stability and predictability in their income.

- Benefits:

- Guaranteed returns: Fixed annuities offer a predetermined interest rate, ensuring a stable income.

- Safety: They are less susceptible to market fluctuations, making them a safer option for conservative investors.

- Considerations:

- Lower returns: Fixed annuities typically offer lower returns compared to variable annuities.

- Inflation risk: The purchasing power of fixed payments may decrease over time due to inflation.

b. Variable Annuities

Variable annuities enable investors to distribute their premiums across various investment choices, including stocks, bonds, and mutual funds. The income from these annuities can vary depending on how the selected investments perform.

- Benefits:

- Potential for higher returns: Variable annuities offer the opportunity for growth based on market performance.

- Flexibility: Investors can adjust their investment allocations to align with their risk tolerance and financial goals.

- Considerations:

- Market risk: The value of the annuity can decline if the underlying investments perform poorly.

- Higher fees: Variable annuities often come with higher fees, including management fees and surrender charges.

c. Indexed Annuities

Indexed annuities blend characteristics of both fixed and variable annuities. They provide a guaranteed minimum return while offering the chance for growth tied to a particular market index, like the S&P 500.

- Benefits:

- Growth potential: Indexed annuities can provide higher returns than fixed annuities if the linked index performs well.

- Downside protection: They typically include a guaranteed minimum return, protecting investors from market losses.

- Considerations:

- Cap on returns: Indexed annuities often have caps on the maximum returns, limiting potential gains.

- Complexity: The structure of indexed annuities can be complicated, making it essential to understand the terms and conditions.

d. Immediate Annuities

Immediate annuities begin making payments to the annuitant right away, usually within a month of purchase. They are typically funded with a lump sum and are ideal for individuals who need immediate income.

- Benefits:

- Quick income: Immediate annuities provide a fast and predictable income stream.

- Simplicity: They are straightforward products, making them easy to understand.

- Considerations:

- Irrevocable: Once purchased, immediate annuities cannot be changed or canceled, limiting flexibility.

- Limited growth potential: Immediate annuities do not offer investment growth, so they may not keep pace with inflation.

e. Deferred Annuities

Deferred annuities allow individuals to invest their money for a certain period before receiving payments. They can be funded with a lump sum or through periodic contributions and are ideal for long-term financial planning.

- Benefits:

- Tax-deferred growth: Earnings on deferred annuities grow tax-deferred until withdrawals are made, allowing for potential compounding.

- Flexibility: Investors can choose when to start receiving payments, making them suitable for retirement planning.

- Considerations:

- Surrender charges: Withdrawals made during the surrender period may incur penalties.

- Delayed income: Payments are not received until the specified deferral period ends, which may not suit everyone’s financial needs.

3. Choosing the Right Annuity Type for You

When selecting an annuity type, consider the following factors:

a. Financial Goals

- Determine your primary financial goals, such as retirement income, wealth preservation, or investment growth. Different annuity types cater to different objectives.

b. Risk Tolerance

- Assess your risk tolerance and investment preferences. If you prefer stability and predictability, fixed annuities may be more suitable. If you’re open to market fluctuations for potential growth, consider variable or indexed annuities.

c. Time Horizon

- Consider your time horizon for retirement or income needs. Immediate annuities are ideal for those needing quick income, while deferred annuities are better for long-term planning.

d. Fees and Expenses

- Review the fees associated with each annuity type. Higher fees can erode returns, so it’s essential to understand the costs involved in your chosen product.

4. Conclusion

In conclusion, understanding annuity types is essential for making informed financial decisions regarding your income stream. Whether you choose fixed, variable, indexed, immediate, or deferred annuities, each type offers unique benefits and considerations tailored to different financial goals and risk tolerances.

Before making a decision, take the time to assess your personal financial situation, goals, and preferences. Consulting with a financial advisor can also provide valuable insights and help you navigate the complexities of annuities, ensuring you choose the right product for your long-term financial security. By making informed choices about annuities, you can create a reliable income stream that supports your financial well-being throughout retirement and beyond.